America is short on homes.

There are 4.7 million fewer housing units than families in the United States, according to a recent report from the real estate website Zillow. And this shortage is getting larger over time, in part because the pace of construction has slowed over the past two decades.

Dwellings are especially scarce — and thus, unaffordable — in places where economic opportunities are plentiful. As a result, the housing shortage hasn’t just fueled displacement and inflation but also stymied economic growth and social mobility. It is arguably the single biggest economic problem in America today.

The Yes In My Backyard (or “YIMBY”) movement seeks to solve it. This faction — a loose constellation of advocacy groups, think tanks, and intellectuals — is animated by one basic observation: America’s housing shortage is mandated by law.

Zoning rules prohibit the construction of apartment buildings on roughly 75 percent of America’s residential land. Throughout much of this territory, land-use laws effectively require all single-family homes to be spacious (and thus, pricey to build or buy). Even in city centers, parking mandates often make multi-family housing financially or physically nonviable.

And these are just three of the more conspicuous ways that regulations constrain housing supply.

YIMBYs have therefore implored local and state governments to relax regulatory restrictions on housing development. The movement has won significant reforms in Minnesota, California, and Montana, among many other states. And with the publication of Ezra Klein (a Vox co-founder) and Derek Thompson’s best-selling book Abundance — a manifesto for YIMBYism and adjacent causes — the quest to loosen land-use laws has attained newfound prominence.

It has also attracted much criticism.

On the left, some hesitate to blame any major social problem on excessive regulation. And they have raised a number of complaints with YIMBYism, most of which are unsound. For example, many contend that upzoning actually raises rents and fuels displacement — an intuition that doesn’t withstand empirical scrutiny.

But there is one left-wing critique of YIMBYism that’s partly right.

What YIMBY skeptics get (half) right

Much YIMBY skepticism is rooted in an accurate observation: Investing in a new housing development is a dicey proposition.

If you park your wealth in an S&P 500 index fund, then your risk is diversified, your holdings can be instantly converted to cash, and you don’t need to take on debt to make your investment pay off.

Developing a real estate project offers none of these advantages. Rather, to get a new apartment building off the ground, a developer must make a big bet on the future value of a single asset, tie up their capital in that project for years, and take out loans to finance construction. To be worth the gamble, the expected return on that building needs to be substantial.

And this is one reason why YIMBY skeptics think land-use reform won’t work: Making it legal to build abundant housing isn’t the same as making it lucrative to do so. If developers ever produced enough apartments to bring down rents — and thus, their own returns — then they would simply stop building.

This view is largely mistaken. It ignores the fact that land-use reform lowers the cost of building — and thus, the minimum rent or home price necessary for a given development to pay off. According to a 2022 report, 40.6 percent of the cost of developing a multi-family housing project can be attributed to regulations. Many of these rules are necessary. But others are not.

Nevertheless, the anti-YIMBYs are gesturing in the general direction of a valid point: Land-use rules aren’t the only constraint on homebuilding’s profitability.

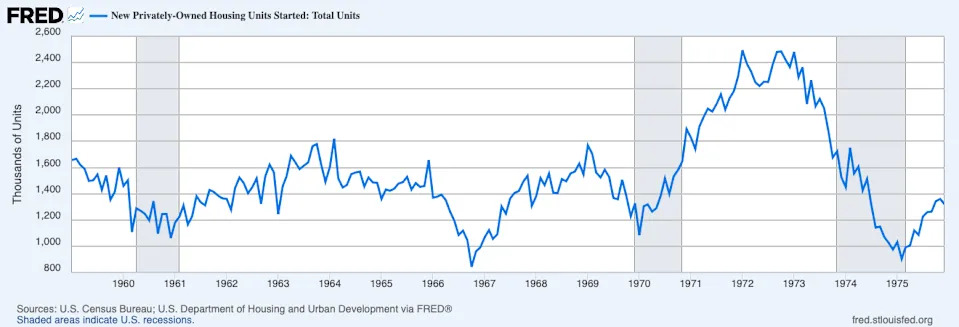

America’s housing sector never recovered from 2008

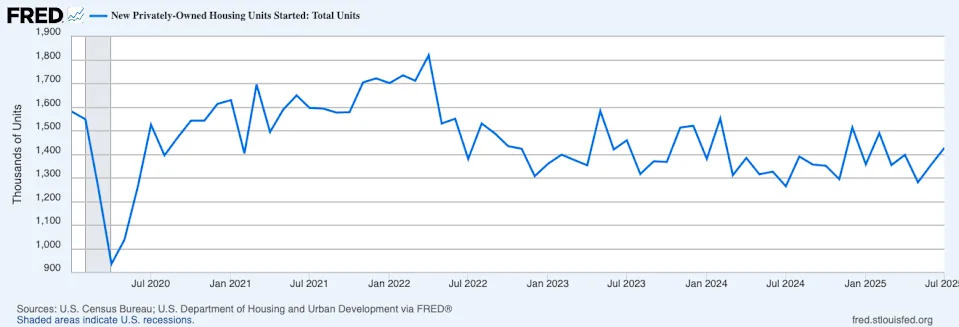

There’s an easy way to see that land-use laws aren’t the sole impediment to homebuilding: Look at a chart of US housing units started since 2000.

American municipalities didn’t suddenly enact radically stricter zoning laws in 2006. So, red tape can’t explain why housing starts abruptly plunged the following year — nor can it fully account for why they’ve remained depressed ever since.

Of course, the late-aughts housing collapse was caused by the subprime mortgage crisis and Great Recession. Given the extraordinary nature of these events, there are limits to what we can learn from the housing bust that coincided with them. Everyone agrees that economic crises are bad for homebuilding and should be avoided. But that doesn’t tell us how to generate housing in normal times.

The more instructive question is why housing production never returned to its pre-crisis peak, even amid the strong economy of 2019 or the post-Covid boom.

Land-use rules could be part of the answer. Density restrictions actually did become more widespread between 2006 and 2018, according to the Wharton Residential Land Use Regulatory Index. And for builders, the financial cost of complying with land-use rules increased by 29 percent from 2011 to 2016.

Nevertheless, the bulk of America’s restrictive zoning regime was in place before the 21st century began. Changes to land-use rules since 2008 haven’t been large enough to fully account for the slowdown in construction.

So, what does?

Builders lack loans, labor, and lumber

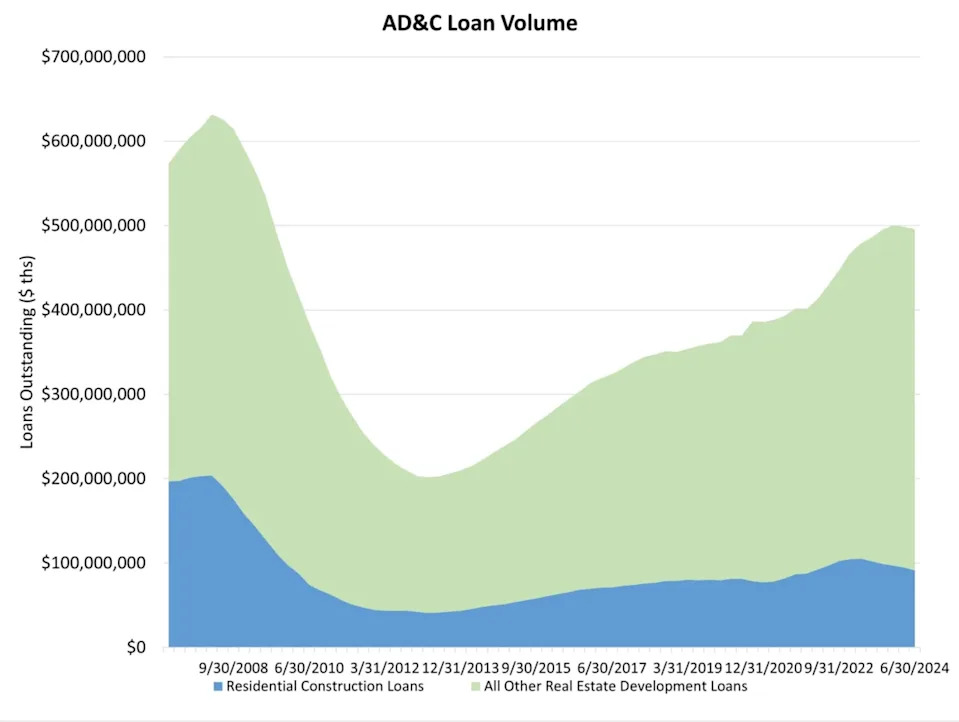

One major factor that affects construction rates — both in general and since 2008 — is the cost and availability of financing.

After the 2008 crash, policymakers made it more expensive for banks to provide construction loans, so as to better account for the risks of such lending. For homebuilders, this made credit more expensive and less accessible. Between 2008 and mid-2024, the dollar value of all residential construction loans fell by 55 percent, according to data from the National Association of Homebuilders.

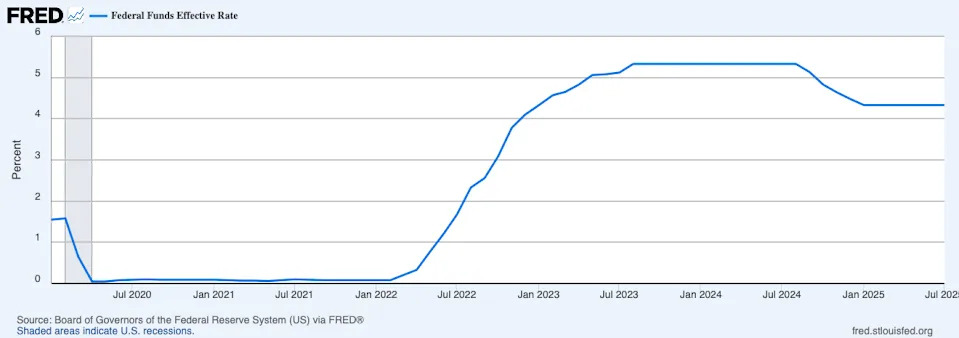

Of course, Federal Reserve policy also has a huge influence. For more than a decade after the Great Recession, low interest rates tempered builders’ financing challenges. Once the Fed started hiking rates in 2022 to combat inflation, however, construction quickly slowed.

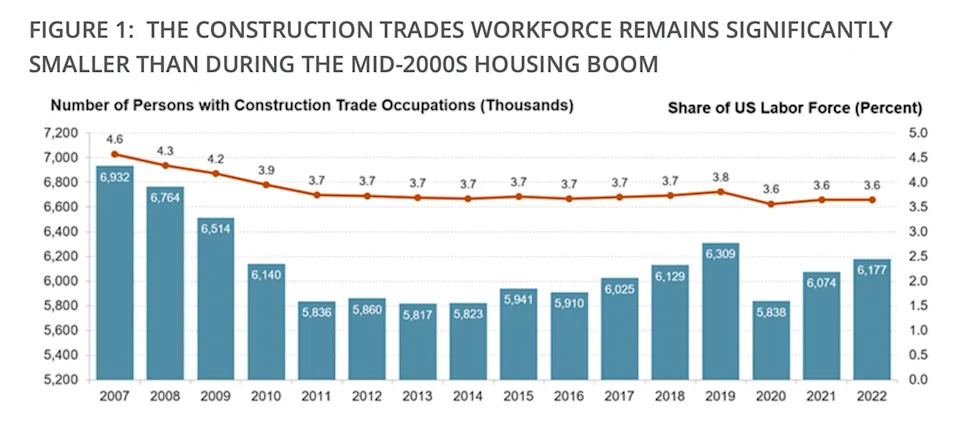

Elevated credit costs haven’t been the only constraint on homebuilding since 2008. Construction labor has also been in short supply.

The Great Recession devastated America’s construction workers. The sector bled nearly 1 million jobs between 2007 and 2011. Many laborers responded by changing fields, retiring, or returning to their home countries. And homebuilders have struggled to replace them, as younger generations have proven harder to recruit and foreign-born trades workers have been immigrating at lower rates.

This shortage of construction workers doesn’t just increase builders’ labor costs (a development that at least has the benefit of boosting wages). It also forces developers to forgo or delay projects that offer an attractive return even with a high wage bill, simply because no skilled workers are available.

Finally, the costs of lumber and other materials have also surged since 2008. The Great Recession shuttered many North American sawmills. When lumber demand recovered in the mid-2010s, a smaller industry struggled to keep up. Then, President Donald Trump’s tariffs made both lumber and metals more expensive for American importers.

In the view of Robert Dietz, chief economist at the National Association of Homebuilders, these forces would perpetuate America’s housing shortage, even under ideal land-use rules.

“If you solve the zoning issue, the labor issue becomes the binding constraint,” Dietz told me. “I do sometimes get a little frustrated when I see a thinktanker say, ‘Okay, if we fix the zoning issue, it’s going to be off to the races.’ No. There’s no single simple, scalable solution that we have to work on all of these challenges.”

A more complete solution to the housing crisis, very hazily sketched

It’s clear that any comprehensive plan for housing abundance must include far more than land-use reform. I don’t have the space or expertise to fully detail such a plan. But I’ll throw out a few ideas, to give you some sense of its shape.

On the financing front, there are many different ways to spur more housing investment.

One is for the government to directly bankroll development itself. Private investors will never offer capital to homebuilders at below-market rates, out of a recognition that society as a whole would be better off with more housing. But municipalities can.

Specifically, local governments can provide favorable financing to multi-family housing projects, in exchange for a cut of future rents. And once that rental income starts flowing, the government can reinvest this revenue into new buildings, in a self-sustaining cycle. Montgomery County, Maryland, has already pioneered this approach to public housing finance, and many other municipalities are considering similar policies.

The federal government could also create new loan programs aimed at stabilizing construction rates. For example, whenever housing starts fall beneath some minimum desired level, the government could start providing cheap, 50-year, fixed-rate mortgages to multi-family housing developers.

Tax policy can further channel capital toward housing. One way to do this is through an accounting rule called “accelerated depreciation,” which allows investors to claim that their apartment buildings are losing value faster than they actually are — and to use those paper losses to shrink their tax bills.

These policies may work best in tandem. The largest housing booms in American history have come when the government reduced the cost of credit and increased public subsidies for housing production.

In the late 1960s, Congress gave below-market credit to builders of affordable rental housing and made accelerated depreciation rules more generous, while the Fed slashed interest rates. A multi-family housing boom larger than any seen before or since ensued (until economic conditions deteriorated in 1973, and the government responded by raising rates and freezing subsidies).

Likewise, in the early 1980s, the Reagan tax cuts established the most aggressive accelerated depreciation rules in history. This, combined with falling interest rates, spurred a surge in multi-family housing construction — which slowed immediately after Congress pared back real estate’s tax advantages in 1986.

Meanwhile, to combat the shortage of construction labor, the government could expand immigration opportunities for skilled trades workers and increase funding for vocational training. To reduce materials costs, it could lift America’s high tariffs on lumber, copper, steel, and other housing inputs.

Policymakers could also try to increase productivity in the construction sector, which has been stagnant for half a century. By adjusting and synchronizing local building codes, the government could make it easier to efficiently produce sections of housing in factories, a process known as modular construction.

Of course, increasing housing production cannot ensure universal affordability. It will never be profitable to sell shelter to the indigent. So no housing agenda is complete without policies that increase the ability of poor and working Americans to make rent, whether through cash transfers, rental subsidies, or social housing.

Why YIMBYs are still right

All this said, I still think YIMBYs are right to prioritize land-use reform. The movement should not (and does not) advocate exclusively for regulatory change. But focusing on that dimension of the problem makes sense, for two reasons.

First, land-use overregulation is a leading cause of housing scarcity and unaffordability. Homebuilding booms and busts may coincide with shifts in financial conditions. But restrictive zoning caps every peak in the housing cycle and deepens every valley.

Second, it costs less than nothing to remove unnecessary constraints on homebuilding. Providing equity, subsidized loans, or tax breaks to the housing sector imposes a fiscal price. So does building social housing. This doesn’t mean that those things aren’t worth doing. But it makes doing any of them at scale politically challenging — especially at the municipal level, where deficit spending is more difficult.

By contrast, land-use reform typically increases municipal revenue: If you legalize apartment buildings, then more will typically go up — which then automatically increases the amount of property taxes you collect. A city can then use those funds to bankroll public developer programs, social housing, or rental subsidies. In this way, land-use reform makes the other dimensions of the housing crisis easier to address.

Put simply, cities are currently going out of their way to make housing scarce and unaffordable. A man who dreams of becoming a concert pianist might need to make many costly investments (such as buying a piano and lessons) to realize that goal. Yet if that man also compulsively sticks his hands into whirring blenders, he’d be well-advised to focus on not doing that first, before worrying about his ambition’s more costly requirements. Asking cities to abandon analogous forms of self-sabotage is a logical starting point for broader reform.

Comments